Healthcare in America Series III – Part 2 Invisible Risk Carriers

“Welcome back to Healthcare in America.

In the last episode, we said something simple but important: risk in healthcare does not disappear. It moves.

Today, we’re going to look at where it lands.

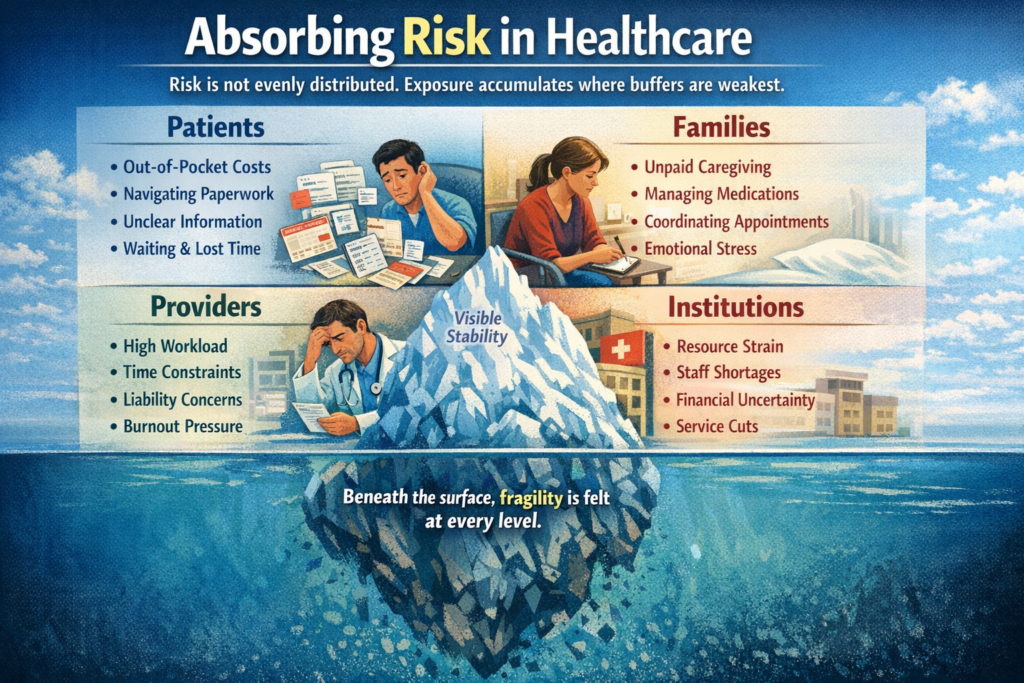

Risk is rarely distributed evenly. Exposure tends to accumulate where buffers are weakest. Some individuals and institutions are better positioned to absorb volatility. Others are not. And the distribution is often quiet — not announced, not debated — just experienced.

Patients are often the first visible absorbers of risk.

Financial exposure can begin long before insurance activates. Deductibles, copayments, and uncovered services create uncertainty before treatment even starts. But financial risk is only part of it.

There is navigational risk — referrals, approvals, coverage rules, and paperwork that must be managed correctly. A missed form or misunderstood instruction can delay care. Informational risk compounds this: patients frequently operate without full clarity about what is covered, what is authorized, or what will happen next.

There is also time risk. Waiting for appointments, coordinating schedules, losing wages during illness — these pressures rarely appear in formal accounting, but they are real exposures.

Families absorb risk as well.

When care transitions from hospital to home, coordination becomes informal. Someone manages medications. Someone schedules follow-ups. Someone interprets discharge instructions under stress. This labor is unpaid, often unrecognized, and structurally necessary. Without it, outcomes decline.

Families also absorb emotional uncertainty. They stabilize environments while waiting for results, while watching for symptoms, while navigating systems that were not designed for clarity.

Providers carry a different kind of exposure.

Clinical risk is inherent in medicine. But modern practice also carries moral and structural risk. Practicing under constraint — limited time, limited staffing, insurance limitations, documentation demands — forces tradeoffs. Liability exposure exists alongside ethical strain. Burnout, in this context, is not simply fatigue. It is accumulated tension between professional obligation and structural limitation.

Institutions absorb risk too.

Hospitals manage volume volatility — unpredictable surges and declines. Rural facilities operate with thin margins and limited redundancy. Workforce shortages increase fragility. Service lines close not necessarily because care is unneeded, but because stability requires contraction somewhere.

On paper, systems can appear stable. Metrics may show balance. But stability at one layer can conceal fragility at another.

This episode does not rank these exposures. It does not assign blame or prescribe reform. It simply observes distribution.

Risk pools where protection is thin.

In the next episode, we’ll look at what happens when that pooled exposure accumulates over time — and how quiet redistribution can eventually reshape entire communities.

For now, the important recognition is this:

When risk moves, it does not vanish.

It settles somewhere.

Often quietly.”

Comments are Disabled