In our last series, we looked at urgency — what happens when care can’t wait, when decisions compress, and when someone must act before clarity arrives.

Now we’re going to step back from the moment of crisis and look at something quieter, but just as powerful: risk.

Before we talk about money, before we talk about policy, before we debate systems — we need to understand something fundamental.

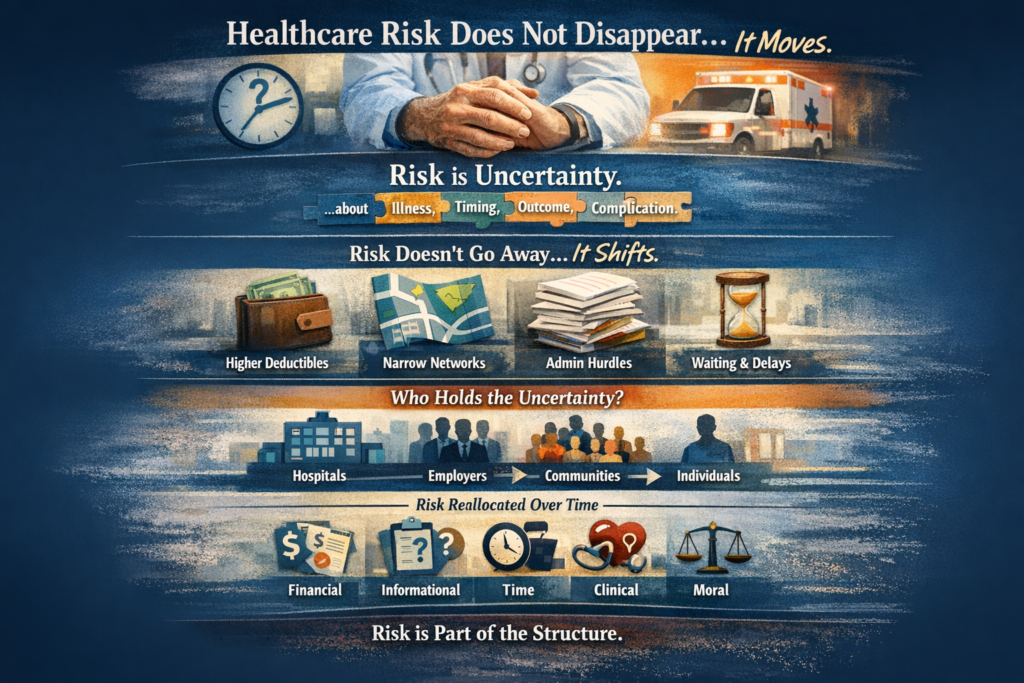

Healthcare risk does not disappear.

It moves.

Risk is not the same thing as cost. Cost is what shows up after something happens. Risk is the exposure that exists before it happens. It is uncertainty — about illness, about timing, about outcome, about complication.

No healthcare system eliminates uncertainty. At best, it redistributes it.

Illness is inherently unpredictable. Some conditions are manageable. Others escalate. Some recoveries are smooth. Others are not. Systems exist to absorb and manage that unpredictability — but they do not erase it.

So the question becomes: who holds the uncertainty?

Historically, risk has sat in different places. Hospitals once absorbed more uncompensated variability. Employers buffered insurance volatility. Communities bore collective responsibility for certain types of care. That arrangement was never perfect, and we don’t romanticize it. But distribution has always shifted over time.

Today, risk often moves quietly.

It can move through higher deductibles — increasing the financial exposure before insurance begins to absorb cost.

It can move through narrower provider networks — limiting flexibility when care is needed.

It can move through administrative complexity — preauthorizations, coverage rules, and paperwork that shift informational burden outward.

It can move through time — waiting, navigating, coordinating.

None of these mechanisms are inherently malicious. They are structural adjustments designed to stabilize institutions. But when systems stabilize themselves, exposure does not vanish. It relocates.

And risk is not singular. It takes multiple forms.

There is financial risk — the possibility of unexpected bills or gaps in coverage.

There is informational risk — not knowing what is covered, what is approved, or what is required.

There is time risk — delays that affect work, income, or progression of illness.

There is clinical risk — the uncertainty of outcome itself.

And there is moral risk — borne by providers who must practice within constraints that limit what they can offer.

When risk moves to individuals, it is often described in the language of responsibility. We hear phrases like “consumer engagement” or “skin in the game.” But exposure and empowerment are not the same thing. Responsibility can feel like choice — but sometimes it is simply proximity to uncertainty.

This is not a debate about political models. It is not an argument for or against any specific reform. It is an observation.

Risk in healthcare is structural.

And structure determines stability.

In the next episode, we’ll look more closely at who absorbs that risk most quietly — and what happens when exposure accumulates beneath the surface.

Comments are Disabled