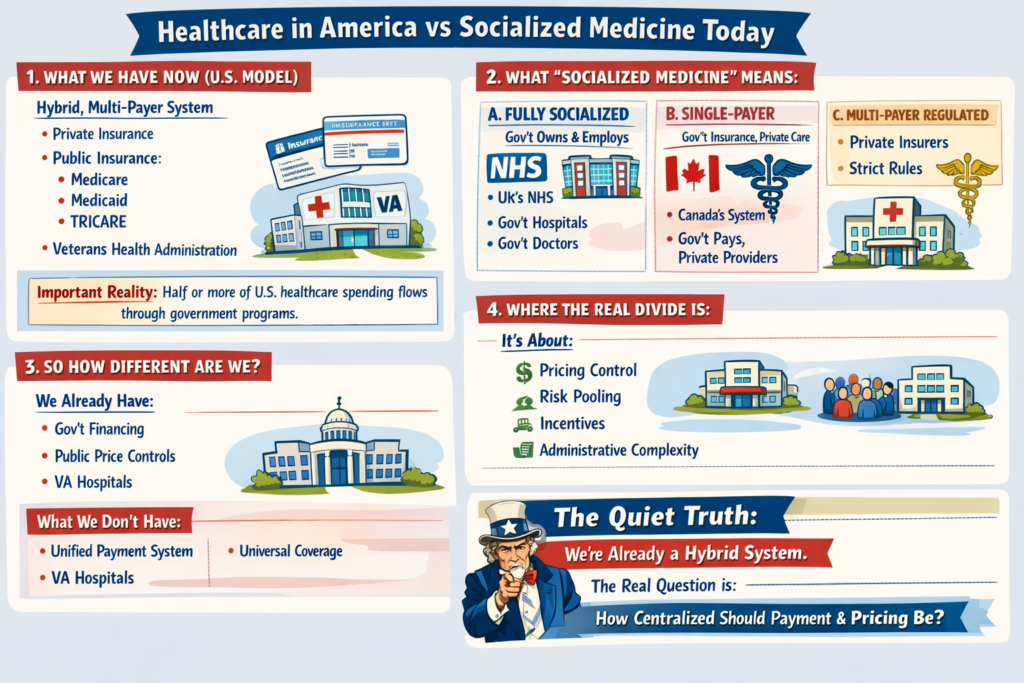

Healthcare in America vs Socialized Medicine Today

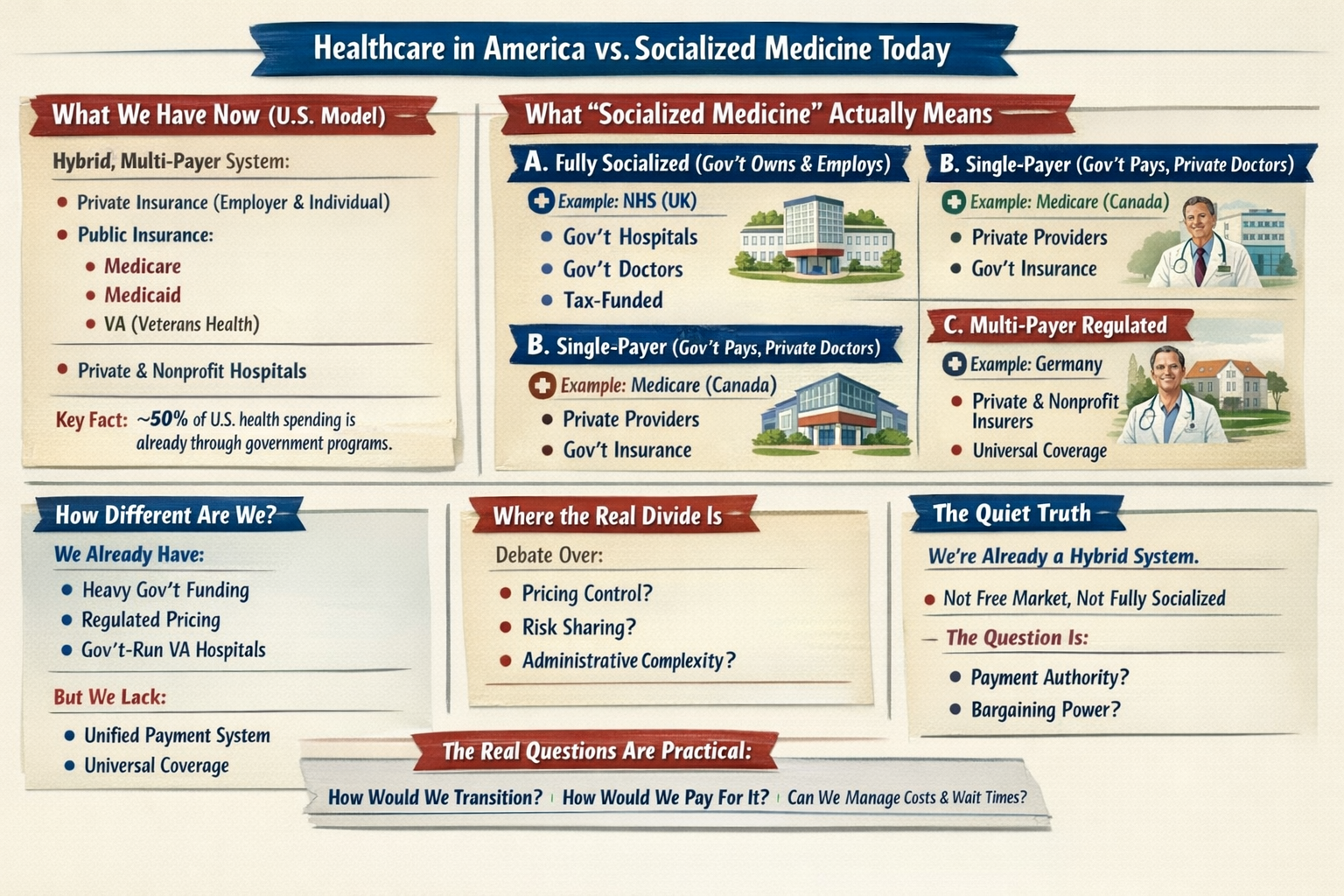

1. What We Have Now (U.S. Model)

The U.S. system is a hybrid, multi-payer system:

-

Private insurance (employer-based and individual market)

-

Public insurance:

-

Medicare

-

Medicaid

-

TRICARE

-

Veterans Health Administration

-

-

Private hospitals (mostly nonprofit, some for-profit)

-

Private physician practices (increasingly consolidated)

Important reality:

Roughly half or more of U.S. healthcare spending already flows through government programs. We are not a pure market system. We are a complex blend.

2. What “Socialized Medicine” Actually Means

People often use “socialized” loosely. There are actually three different models internationally:

A. Fully Socialized (Government Owns & Employs)

Example: National Health Service in the UK

-

Government owns hospitals

-

Doctors are government employees

-

Government sets budgets directly

-

Care funded through taxes

That’s true “socialized medicine.”

B. Single-Payer (Government Pays, Private Providers Deliver)

Example: Medicare (Canada’s system)

-

Private hospitals & doctors

-

Government is the main insurer

-

One public payment system

-

Funded via taxes

This is not government-run hospitals — it’s government-run insurance.

C. Multi-Payer Regulated System

Example: Statutory Health Insurance

-

Private and nonprofit insurers

-

Strict national rules

-

Price controls

-

Universal coverage mandate

3. So How Different Are We?

Structurally:

-

We already have heavy government financing.

-

We already regulate pricing in public programs.

-

We already operate large government-run care systems (VA hospitals).

-

We already subsidize private insurance through tax exclusions.

What we don’t have:

-

A unified payment structure

-

National price controls across the board

-

Universal automatic coverage

-

Simplified billing

The biggest structural difference isn’t just “who pays.”

It’s:

-

Fragmentation

-

Administrative layering

-

Pricing freedom in private markets

-

Employment-tied insurance

4. Where the Real Divide Is

The debate isn’t simply:

Private vs Socialized.

It’s about:

-

Who controls pricing?

-

How risk is pooled?

-

How incentives are aligned?

-

How much administrative complexity is tolerated?

Even a “socialized” system still rations care — just differently (wait times vs cost-sharing).

Even our current system has price controls — just unevenly applied.

5. If the U.S. “Moved Toward Socialized” — What Would Actually Change?

Not necessarily hospital ownership.

More likely changes would include:

-

Centralized bargaining power

-

Uniform reimbursement rates

-

Elimination of employer-based insurance

-

Tax-based funding instead of premium-based funding

-

Dramatically reduced administrative overhead

-

Reduced insurer role

The money flow changes.

The power centers shift.

Administrative structure simplifies.

But doctors would still practice medicine.

Hospitals would still exist.

Care would still be rationed — just through different mechanisms.

6. The Quiet Truth

We are already halfway between models.

The U.S. system is not a free market.

It is not socialized.

It is a layered hybrid with competing incentives.

The question isn’t:

“Would we become socialized?”

The real question is:

“How centralized do we want payment and pricing authority to be?”

That’s a structural debate — not just a funding debate.

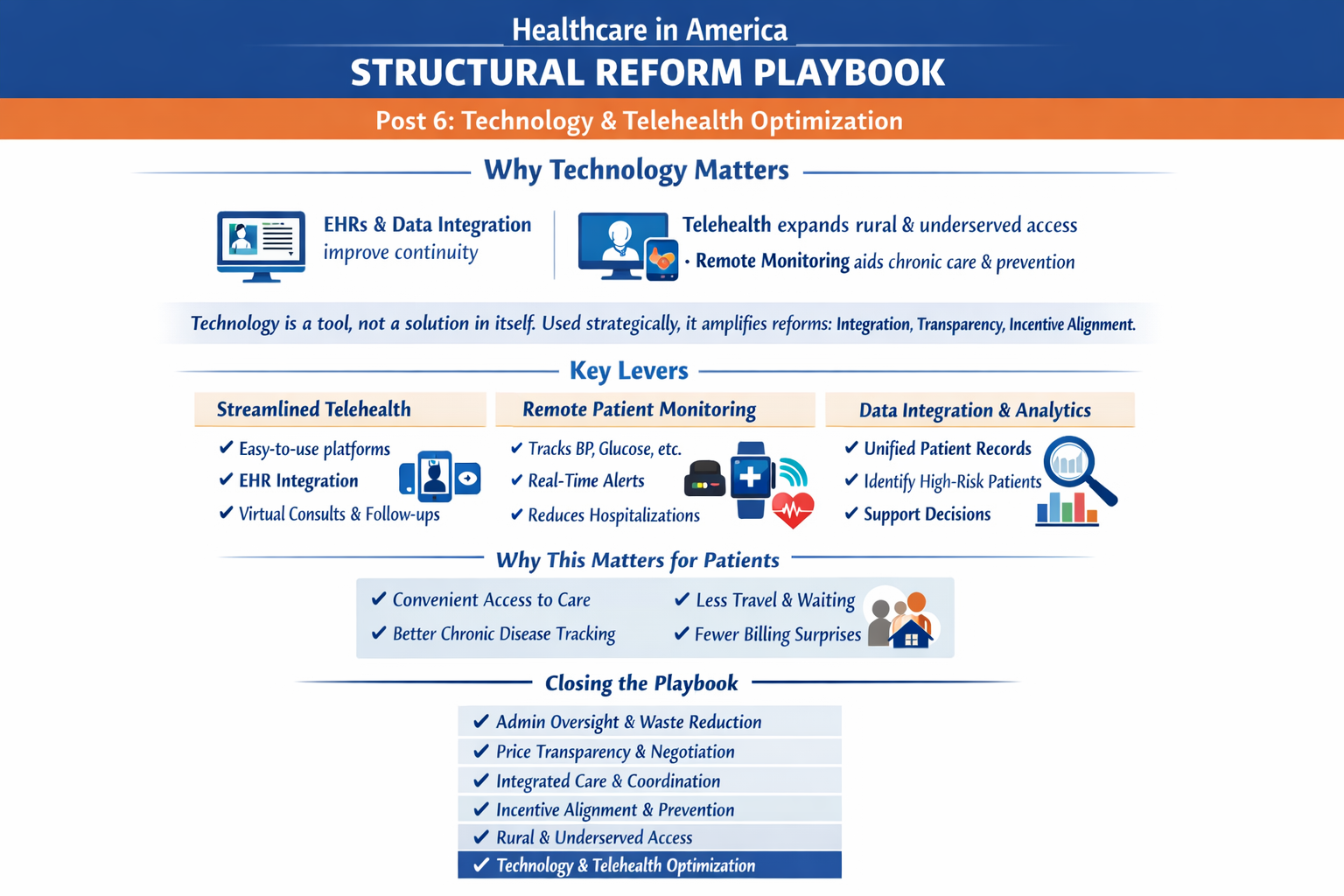

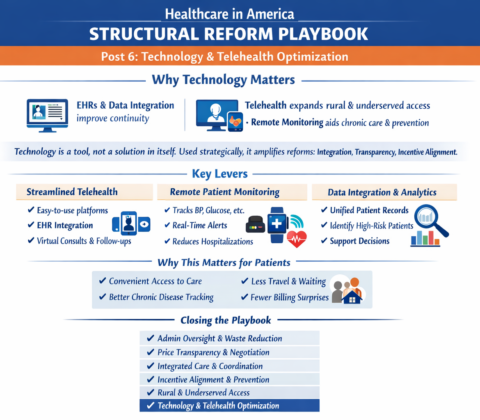

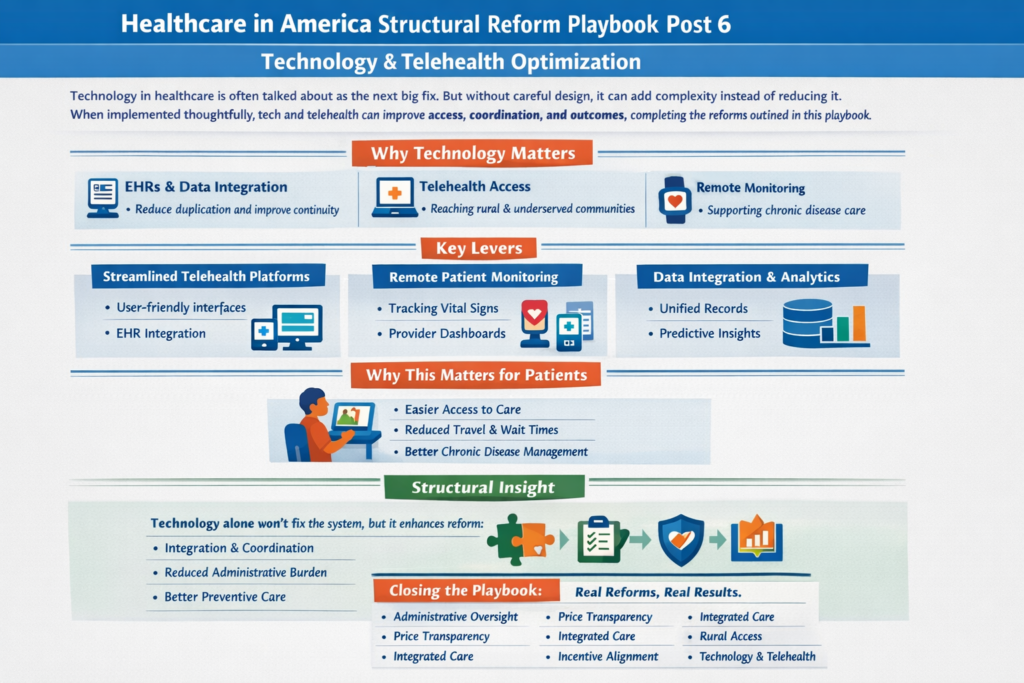

To go deeper, we have to explore:

-

What would actually happen to costs?

-

What happens to innovation?

-

What happens to wait times?

-

Or what a realistic transition would look like?

The real questions aren’t ideological. They’re mechanical:

A Pivot Opportunity on America’s Mental Health Crisis – Redirecting Priorities from Endless War

Elon,You’ve already highlighted failures in mental health policy—deinstitutionalization left untreated severe cases on the streets, fueling homelessness, addiction, crime, and chaos (your “Make Asylums Great Again” posts in Feb 2026 nailed the critique of that 20th-century cost-cutting disaster). You’ve been open about personal struggles too (prescription ketamine for dark states, calling out “mental rabies” in violent offenders who need containment/treatment, not release).

The current hypocrisy is glaring and worsening: The Iran war (started late Feb 2026) is burning ~$1 billion/day (Pentagon briefed Congress on $11.3B+ in first 6 days; estimates now push $12–18B+ cumulative by mid-March, per CSIS/Reuters/NYT). That’s endless foreign escalation with no clear end, spiking gas prices and hurting Americans at home—while behavioral health funding gets squeezed (billions cut/reversed in SAMHSA grants under recent efficiencies).

A subtle distance from the current admin’s trajectory (less close proximity to avoid shrapnel from backlash) could open huge ground for you to lead on this domestically. Champion modern psychiatric treatment centers/recovery campuses (avoid “asylums” stigma—frame as humane, evidence-based facilities with safeguards, voluntary where possible, mandatory for severe threats). Tie it to protecting families/communities from exploitation, trauma, addiction cycles—subtly “shines” your image amid any lingering noise (e.g., old Epstein file smears).

Bring in Bezos, Zuckerberg, Ellison (Oracle) for a consortium: Announce an initial $19.5B fund (roughly 2–3 weeks of current war burn—people can do the math). Position it as:

Not replacing DEA street-level enforcement (that’s federal law job).

Funding treatment infrastructure: beds, crisis units, integrated SUD/mental health care, recovery housing, peer programs.

“Giving back”—this money originated from American taxpayers; redirecting a fraction to heal at home instead of endless abroad conflicts.

You have the platform (X), cash, and disruption cred to make this viral and bipartisan—addressing blue-city street crises and rural opioid/mental health gaps without heavy ideology. It aligns with your existing views, scales like your big missions, and could force national conversation/pressure for reallocations.

Worth considering? The timing (lame-duck dynamics, midterm/economic pain building) might be right.

No pressure—just an idea from a purple independent who’s tired of misplaced priorities.

Share this:

Like this: